You found a therapist you want to work with, and then you looked at the cost, and now you're wondering whether your insurance will cover any of it. That moment of hesitation is one of the most common reasons people delay starting therapy. And honestly, the insurance system doesn't make it easy to figure out.

In my practice, this is one of the most common questions new clients have, and it's simpler than most people think. So let's walk through this together, in plain language, because it's more straightforward than it seems once you know what to ask and where to look.

Every plan is different (really)

Here's the thing about insurance: two people with the same insurance company can have completely different coverage because they're on different plans through different employers. So while this article gives you a general framework, the only way to know your specific situation is to call the number on the back of your insurance card and ask.

That one phone call can save a lot of confusion later. And it's worth making before your first session, not after.

In-network vs. out-of-network

An in-network therapist has a contract with your insurance company. They've agreed to a set fee schedule, and your insurance picks up a bigger share of the cost. For you, that usually means a simpler copay and less paperwork.

An out-of-network therapist doesn't have that contract. The upside is more flexibility in how they work: session length, treatment approach, scheduling. The tradeoff is that you'll typically pay the full fee upfront and then seek reimbursement from your insurance company afterward. How much you get back depends entirely on your plan.

What a lot of people don't realize is that many PPO plans have out-of-network behavioral health benefits that are actually pretty decent. Many people get 60 to 80% of the fee reimbursed once they've met their deductible. Others have plans that don't cover out-of-network at all. We won't know until we check.

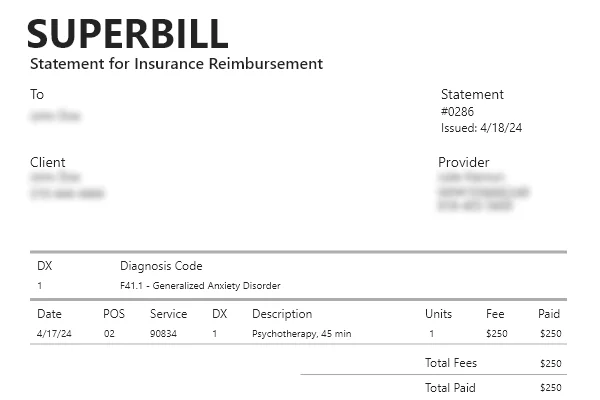

So what is a superbill, exactly?

A superbill is the detailed receipt your therapist gives you after each session. It has everything your insurance company needs to process a claim: the therapist's license number, your diagnosis code, the type of session, the date, and the fee. Think of it as an invoice formatted specifically for insurance. You submit it to your insurance company, and they process it against your out-of-network benefits.

The diagnosis code is the piece that matters most to the insurance company. It tells them what's being treated and why the sessions are medically appropriate.

What to ask your insurance company before you start

It's worth calling your insurance before your first session. Write down the answers and the name of the representative you speak with, since that matters if there's ever a dispute later. Here are the key questions to ask:

- Out-of-network coverage: Do you have out-of-network coverage for a Licensed Marriage and Family Therapist?

- Deductible: What is your out-of-network deductible, and how much have you met so far this year?

- Reimbursement rate: What percentage of the session fee gets reimbursed once you meet that deductible?

- Session limits: Is there a limit on the number of therapy sessions per year?

- Referral requirements: Do you need a referral from your primary care doctor?

Once you have those answers, the picture gets much clearer. You'll know what therapy will actually cost you out of pocket, and you can make the decision that's right for your situation.

Submitting your superbill

The process is simpler than most people expect. Call your insurance company's member services line and ask how they want you to submit. Some companies have an online portal where you can upload it directly. Others want you to fax or mail it.

It helps to submit monthly rather than waiting until the end of the year, since claims can take time to process and it's easier to resolve issues when they're fresh. Keep a copy of everything you send, along with confirmation numbers or emails. And if a claim is denied, don't assume it's final. Call and ask why. Sometimes it's a coding error or a missing piece of information that's easy to fix.

The insurance side of therapy can feel like a lot, especially when you're also dealing with whatever brought you to therapy in the first place. But once that initial phone call is made and the submission process is set up, it becomes routine. And for many people, the reimbursement makes it significantly more affordable to see the therapist who's the right fit, even if that therapist is out-of-network. For more details about fees and logistics, you can visit our frequently asked questions page.

In person and virtual sessions available

If you have questions about how superbills work with my practice or want to get started with therapy, I'm here. You can fill out the contact form below or call me at 818-403-5439. I see clients in person at my Agoura Hills office and virtually anywhere in California, including Westlake Village, Oak Park, Calabasas, Thousand Oaks, Woodland Hills, and Simi Valley.